Award-winning PDF software

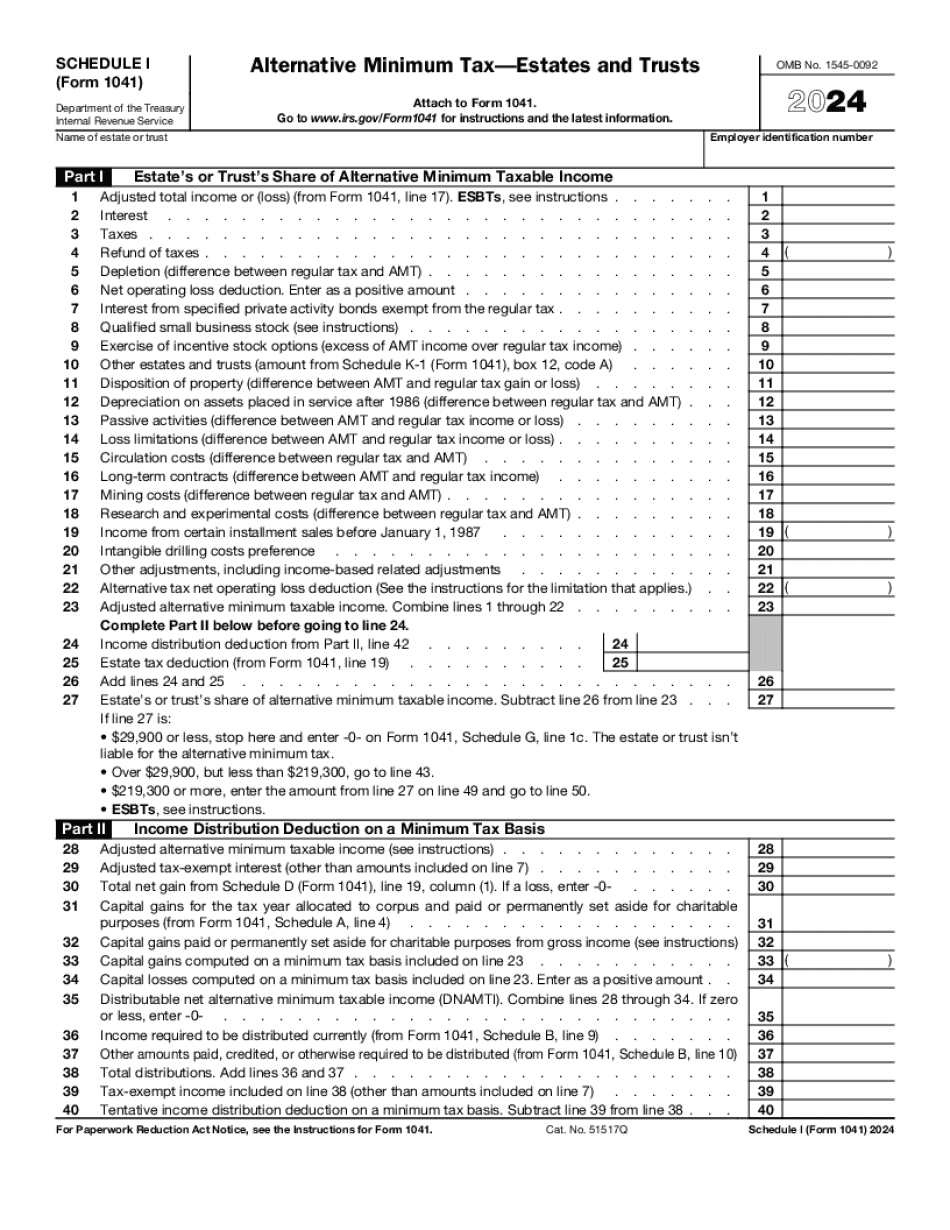

Spokane Valley Washington Form 1041 (Schedule I): What You Should Know

A decedent who owns taxable property in Washington who dies in this State at the time of death, and has not substantially reduced the amount of such property in the course of lifetime, may deduct the portion of the value of the decedent's interest in the property that is greater than or equal to 125,000 and less than or equal to 250,000. A decedent subject to the estate tax under this paragraph, who elects to be treated as a Washington resident for estate tax purposes. A nonresident decedent who lives in our State, who dies in our State, may not file with the Department of Revenue a state estate tax return that would prevent the beneficiary from deducting estate taxes paid to Washington under this paragraph for a period of 10 years beginning 1 year after the decedent's death. The prohibitions do not apply to the state's federal estate tax. A decedent's spouse or a dependent child who qualifies for the child tax credit. A person who is dependent on the decedent under the Alaska codification would not be deemed a dependent if the person also is not subject to the state estate tax under that rule. The estate of a decedent who qualifies under state or federal law as eligible to participate in the estate tax exclusion. Under the Alaska codification, estates are considered eligible for the estate and gift tax exclusion if they are owned by the decedent, or were the subject of a will that includes an estate exclusion for the purpose. A decedent who qualified for the death tax exclusion under an intestacy decree. Under state law, estates may be exempt if they are owned by the decedent and were the subject of a will that included an estate exclusion for the purpose of preventing a tax from being paid. A decedent who was married at the time of his death or died within five years after the marriage. A decedent who qualified for the death tax exclusion under an intestacy decree. Under state law, estates may also be exempt if they were the subject of a will that included an estate exclusion for the purpose of preventing a tax from being paid. A beneficiary under a trust agreement. Under state law, trusts may be exempt if they were the subject of a will that included an estate exclusion for the purpose of preventing a tax from being paid. A decedent at least 55 years of age at the time of his death.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Spokane Valley Washington Form 1041 (Schedule I), keep away from glitches and furnish it inside a timely method:

How to complete a Spokane Valley Washington Form 1041 (Schedule I)?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Spokane Valley Washington Form 1041 (Schedule I) aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Spokane Valley Washington Form 1041 (Schedule I) from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.