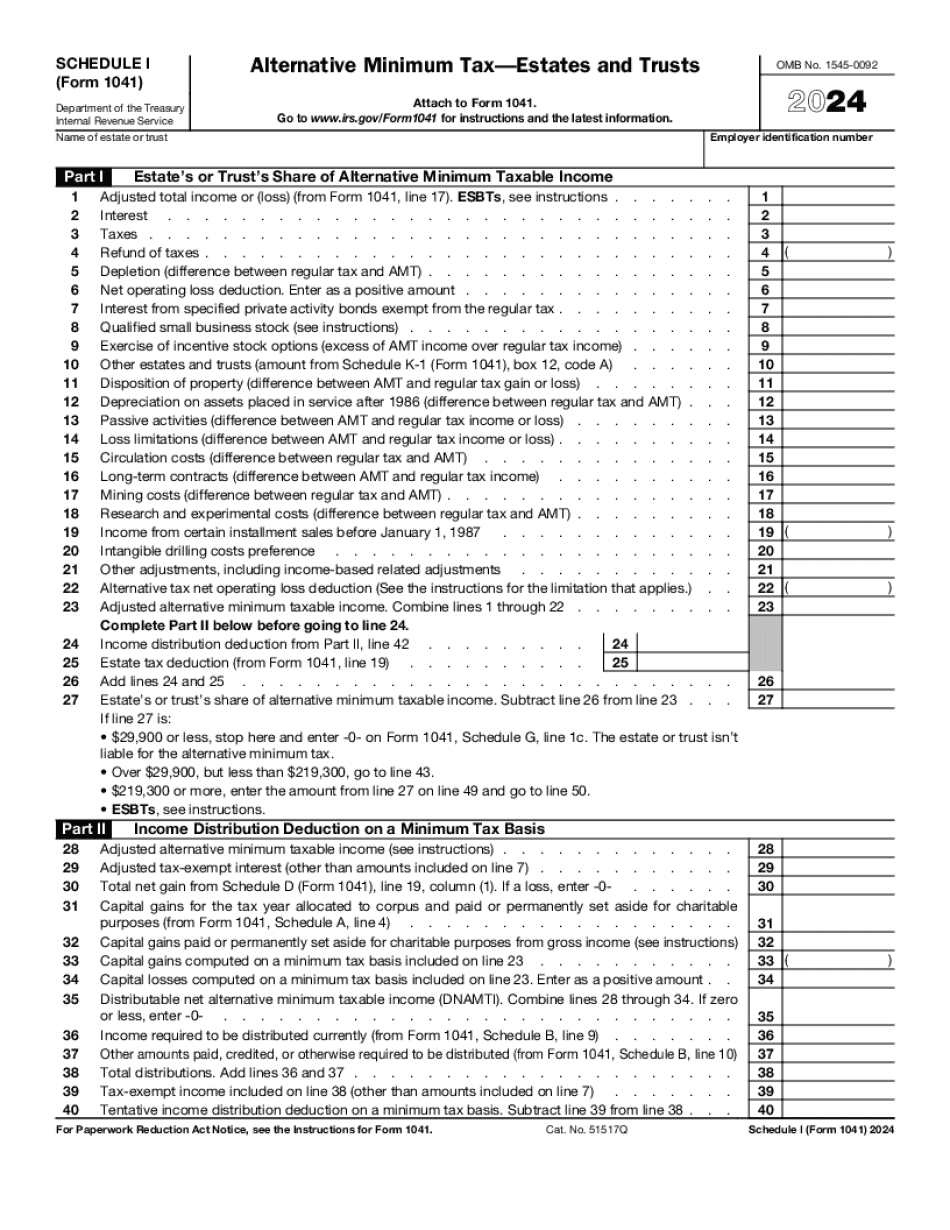

Form 1041 Schedule I

Home

Top Forms

Form 1041 Schedule I

Home

Top Forms

Get

How 1041 Schedule Instructions 2024-2025

Get Form

Home

TOP Forms to Compete and Sign

How 1041 Schedule Instructions 2024

👉

Did you like how we did? Rate your experience!

Rated

4.5 out of

5

stars by our customers

561

Award-winning PDF software

If you believe that this page should be taken down, please follow our DMCA take down process

here

.

Related Content - How 1041 Schedule Instructions 2024

Instructions for Schedule I (Form 1041), alternative minimum ...

Instructions for Schedule I (Form 1041), alternative minimum tax, estates and trusts. Save to Lists · Login to SaveManage List ...

About Schedule I (Form 1041), Alternative Minimum Tax

Jun 8, 2021 — Information about Schedule I (Form 1041), Alternative Minimum Tax - Estates and Trusts, including recent updates, related forms, ...

2017 Form 3800 F3800 - UserManual.wiki

You must attach all pages of Form 3800, pages 1, 2, and 3, to your tax return. OMB No. 1545-0895 ... Enter the amount from Schedule I (Form 1041), line 56 .

Get Form

100%

Loading, please wait

.

.

.